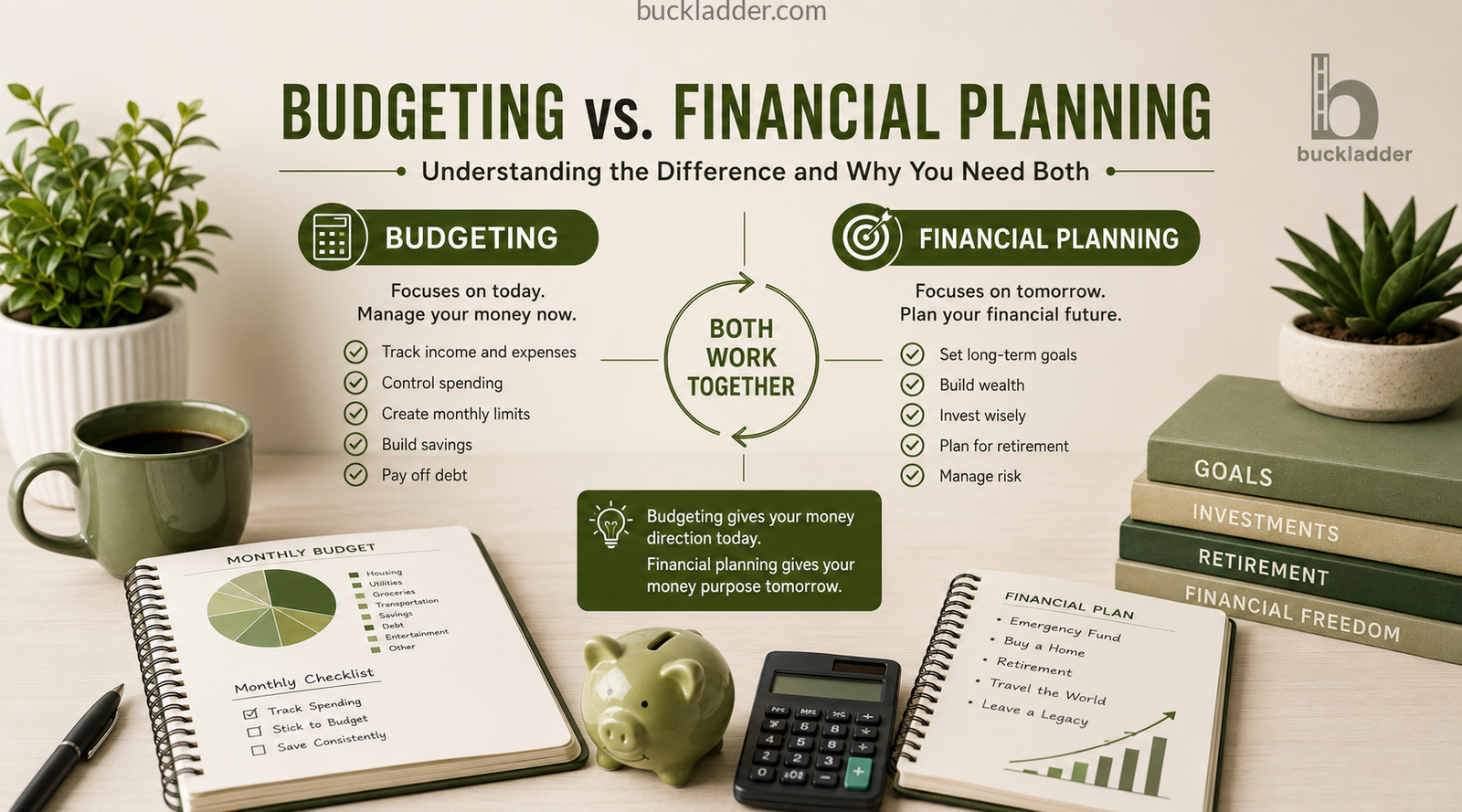

Budgeting vs. Financial Planning: Understanding the Difference and Why You Need Both

Many people use the terms budgeting and financial planning interchangeably.

While they’re closely related, they’re not the same thing.

In fact, confusing the two is one of the biggest reasons people struggle to achieve their financial goals.

Think of it this way:

A budget tells your money where to go today.

A financial plan tells your money where it needs to take you tomorrow.

Both are essential. One manages your current finances, while the other helps shape your financial future.

Let’s explore the differences and how they work together.

What Is Budgeting?

Budgeting is the process of managing your income and expenses over a specific period, usually monthly.

A budget answers questions such as:

- How much money am I earning?

- How much am I spending?

- Where is my money going?

- How much can I save?

- How much debt can I pay off?

A budget focuses on the present.

Its purpose is to ensure your spending aligns with your income and priorities.

Example of a Budget

Monthly Income: $5,000

| Category | Amount |

|---|---|

| Housing | $1,500 |

| Utilities | $250 |

| Groceries | $500 |

| Transportation | $400 |

| Savings | $600 |

| Entertainment | $250 |

| Debt Payments | $500 |

| Miscellaneous | $1,000 |

A budget provides a snapshot of how money is being allocated today.

What Is Financial Planning?

Financial planning is the broader process of creating a long-term strategy for achieving financial goals.

It looks beyond monthly bills and focuses on the future.

A financial plan answers questions such as:

- When can I retire?

- How much should I invest?

- How do I build wealth?

- Can I afford to buy a home?

- How do I fund my children’s education?

- What happens if I lose my income?

Financial planning is about creating a roadmap for the years and decades ahead.

Example of a Financial Plan

Imagine Sarah, age 30.

Her goals include:

- Buying a home within five years

- Retiring by age 60

- Building a six-month emergency fund

- Paying off all debt within three years

- Investing for long-term growth

Her financial plan outlines:

- Savings targets

- Investment strategy

- Debt repayment schedule

- Insurance coverage

- Retirement contributions

- Risk management

Unlike a budget, a financial plan may cover 5, 10, 20, or even 40 years.

The Simple Analogy

Imagine you’re planning a road trip.

Financial Planning Is the Destination

It answers:

- Where are you going?

- How long will it take?

- What route will you follow?

Budgeting Is the Fuel Management

It answers:

- How much gas can you buy?

- How much can you spend each day?

- Can you afford the journey?

Without a destination, fuel management has no purpose.

Without fuel management, you never reach the destination.

You need both.

Key Differences Between Budgeting and Financial Planning

| Budgeting | Financial Planning |

|---|---|

| Short-term focus | Long-term focus |

| Tracks income and expenses | Creates financial goals |

| Usually monthly | Often spans years or decades |

| Focuses on spending | Focuses on wealth building |

| Helps control money | Helps grow money |

| Tactical | Strategic |

Both serve different but complementary roles.

Why Budgeting Comes First

Many people want to invest, retire early, or buy a home.

But none of these goals are achievable without a solid budget.

Budgeting creates the cash flow needed to fund future goals.

Without budgeting:

- Savings become inconsistent

- Debt grows faster

- Financial goals get delayed

- Investment contributions suffer

A financial plan without a budget is like building a house without a foundation.

Why Financial Planning Matters

Some people become excellent budgeters but never create a long-term plan.

They successfully manage expenses but fail to build wealth.

Without financial planning:

- Savings may sit idle

- Retirement may be underfunded

- Investment opportunities may be missed

- Risk management may be overlooked

Financial planning ensures your money has a purpose beyond paying bills.

How Budgeting and Financial Planning Work Together

The most successful people combine both.

For example:

Step 1: Create a Financial Goal

“I want to retire with $1 million.”

Step 2: Build a Financial Plan

Determine:

- Required savings rate

- Investment strategy

- Retirement timeline

Step 3: Create a Budget

Allocate money monthly to:

- Retirement accounts

- Investments

- Emergency savings

The budget becomes the engine that powers the financial plan.

Common Mistakes People Make

Focusing Only on Budgeting

Some people spend years tracking every dollar but never invest or plan for the future.

Result:

Good financial habits but slow wealth accumulation.

Focusing Only on Financial Planning

Others create ambitious retirement plans and investment goals but never manage daily spending.

Result:

Plans remain on paper and rarely become reality.

Ignoring Either One

Both approaches create financial blind spots.

True financial success requires both short-term control and long-term vision.

Which Is More Important?

This question is similar to asking:

“Which is more important, the engine or the steering wheel?”

The answer is both.

Budgeting and financial planning serve different purposes.

Budgeting Helps You:

- Control spending

- Reduce debt

- Build savings

- Improve cash flow

Financial Planning Helps You:

- Build wealth

- Prepare for retirement

- Manage risk

- Achieve major life goals

One supports the present.

The other shapes the future.

Real-Life Example

Consider two friends.

John

- Budgets carefully every month

- Saves money consistently

- Has no financial plan

After 20 years, he has savings but little wealth growth.

Michael

- Has a financial plan

- Invests regularly

- Uses a budget to stay on track

After 20 years, he has built significant wealth and achieved several financial goals.

The difference isn’t income.

It’s having both a budget and a financial plan.

Signs You Need a Budget

You may need a stronger budget if:

- You frequently run out of money before payday

- You carry credit card balances

- You don’t know where your money goes

- Saving feels difficult

Signs You Need a Financial Plan

You may need a stronger financial plan if:

- You have no retirement strategy

- You don’t have long-term goals

- You aren’t investing consistently

- You’re unsure whether you’re on track financially

Building Your Financial Future

The best approach is simple:

- Create a realistic budget.

- Establish meaningful financial goals.

- Build a long-term financial plan.

- Review both regularly.

- Adjust as life changes.

This combination creates financial stability today and financial freedom tomorrow.

Key Takeaways

- Budgeting and financial planning are not the same thing.

- Budgeting focuses on managing current income and expenses.

- Financial planning focuses on achieving long-term goals.

- A budget provides control.

- A financial plan provides direction.

- The most successful financial strategies combine both.

Budgeting helps you manage today’s money.

Financial planning helps you build tomorrow’s wealth.

Together, they create the foundation for lasting financial success.